Understanding the effects of a hard credit pull on your credit score is essential for anyone seeking financial stability and growth. A hard credit inquiry can have lasting consequences that may impact your creditworthiness. Knowing how long a hard credit pull lasts and its implications is crucial for maintaining a healthy financial profile.

Whether you're applying for a new credit card, a mortgage, or even a car loan, lenders often conduct hard credit pulls to assess your creditworthiness. While these inquiries provide valuable insights into your financial behavior, they can also affect your credit score in significant ways.

This article aims to provide a comprehensive guide on how long a hard credit pull lasts, its impact on your credit score, and strategies to manage its effects. By the end, you'll have a clear understanding of how to protect your credit score while navigating the complexities of credit applications.

Read also:Taecyeon Wife A Complete Guide To The Life And Love Of The Kpop Star

Table of Contents

- What is a Hard Credit Pull?

- Hard vs. Soft Credit Inquiries

- How Long Does a Hard Credit Pull Last?

- Impact of Hard Credit Pulls on Your Credit Score

- Factors Affecting Credit Score

- Managing Hard Credit Pulls

- Strategies to Maintain Credit Health

- Common Misconceptions About Hard Credit Pulls

- How to Check Your Credit Report

- Conclusion

What is a Hard Credit Pull?

A hard credit pull, also known as a hard inquiry, occurs when a lender or creditor checks your credit report to evaluate your creditworthiness. This typically happens when you apply for credit products such as loans, credit cards, or mortgages. Unlike soft inquiries, which don't affect your credit score, hard inquiries can have a temporary impact on your credit rating.

Hard credit pulls are recorded on your credit report and remain visible to other lenders. They are a reflection of your financial behavior and can indicate how often you seek new credit. However, it's important to note that not all hard inquiries are created equal. For example, rate shopping for mortgages or auto loans within a specific time frame is treated differently by credit scoring models.

Why Do Lenders Conduct Hard Credit Pulls?

Lenders conduct hard credit pulls to assess your credit history, payment patterns, and overall financial health. This information helps them determine the level of risk associated with extending credit to you. By reviewing your credit report, lenders can evaluate your ability to repay debt and make informed decisions about your application.

- To assess your creditworthiness

- To determine the risk of lending to you

- To verify your financial stability

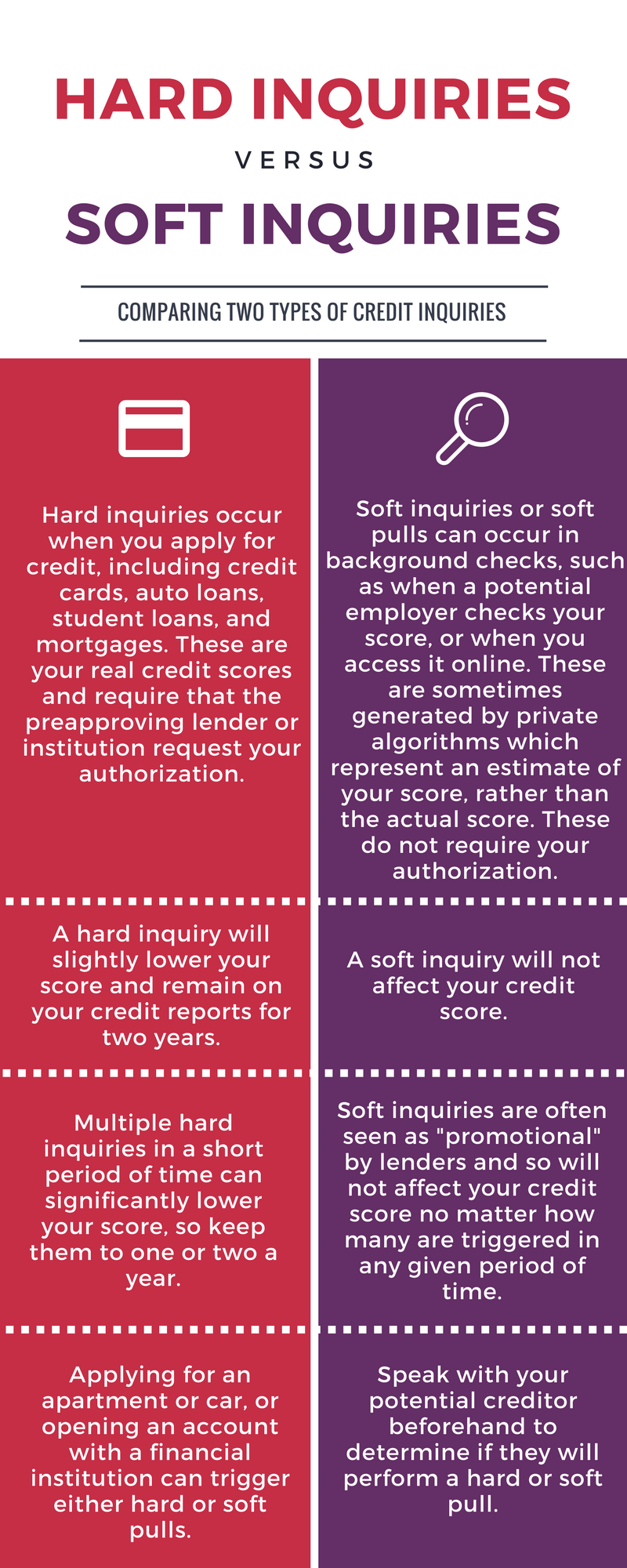

Hard vs. Soft Credit Inquiries

Understanding the difference between hard and soft credit inquiries is crucial for maintaining a healthy credit score. While both types of inquiries involve accessing your credit report, they differ significantly in their impact on your credit profile.

Hard Credit Inquiries: These occur when you actively apply for credit, and the lender checks your credit report to make a lending decision. Hard inquiries can slightly lower your credit score and remain on your credit report for up to two years.

Soft Credit Inquiries: These are initiated by yourself or third parties, such as potential employers or insurance companies, and do not affect your credit score. Soft inquiries are for informational purposes and do not indicate a request for new credit.

Read also:Buscar Kid And His Mom Cctv Video Original A Deep Dive Into The Viral Sensation

Key Differences Between Hard and Soft Inquiries

- Hard inquiries impact your credit score, while soft inquiries do not.

- Hard inquiries are initiated by your application for credit, while soft inquiries are often for background checks or pre-approved offers.

- Hard inquiries remain on your credit report for two years, while soft inquiries are not visible to other lenders.

How Long Does a Hard Credit Pull Last?

A hard credit pull remains on your credit report for up to two years. However, its impact on your credit score typically diminishes after a few months. Most credit scoring models, such as FICO and VantageScore, consider hard inquiries as a minor factor in calculating your credit score. While the inquiry itself may remain visible for two years, its effect on your score is usually short-lived.

It's important to note that multiple hard inquiries within a short period can signal financial instability to lenders. Therefore, it's advisable to limit the number of credit applications you submit unless absolutely necessary.

How Long Does a Hard Inquiry Affect Your Credit Score?

While a hard credit pull remains on your credit report for two years, its impact on your credit score typically lasts for about six months to one year. After this period, the effect diminishes as newer information is added to your credit report. Consistently paying bills on time and managing debt responsibly can help offset any negative effects of a hard inquiry.

Impact of Hard Credit Pulls on Your Credit Score

Hard credit pulls can lower your credit score by a few points, depending on various factors such as your credit history and existing credit accounts. For individuals with a short credit history or limited credit accounts, the impact may be more pronounced. Conversely, those with a long and diverse credit history may experience minimal effects.

Credit scoring models consider multiple factors when evaluating your creditworthiness. While hard inquiries are a factor, they account for a relatively small percentage of your overall score. Other factors, such as payment history, credit utilization, and length of credit history, play a more significant role in determining your credit score.

Factors That Influence the Impact of Hard Credit Pulls

- Length of credit history

- Number of existing credit accounts

- Payment history

- Credit utilization ratio

Factors Affecting Credit Score

Your credit score is influenced by several key factors, each contributing to your overall creditworthiness. Understanding these factors can help you manage your credit profile effectively and minimize the impact of hard credit pulls.

Payment History: This is the most significant factor affecting your credit score, accounting for approximately 35% of your total score. Consistently paying bills on time demonstrates financial responsibility and positively impacts your credit rating.

Credit Utilization: This refers to the amount of credit you're using compared to your available credit limit. Keeping your credit utilization below 30% is generally recommended to maintain a healthy credit score.

Other Key Factors

- Length of credit history

- Mix of credit accounts

- New credit applications

Managing Hard Credit Pulls

While it's impossible to avoid hard credit pulls entirely, there are strategies to manage their impact on your credit score. One effective approach is to limit the number of credit applications you submit within a short period. Additionally, understanding how credit scoring models treat rate shopping can help you make informed decisions.

Rate shopping, or applying for multiple quotes for the same type of loan, is typically treated as a single inquiry by credit scoring models if done within a specific time frame. This allows consumers to compare rates without incurring multiple hard inquiries on their credit report.

Tips for Managing Hard Credit Pulls

- Limit credit applications to only what's necessary

- Shop for rates within a 14-45 day window

- Monitor your credit report regularly

Strategies to Maintain Credit Health

Maintaining a healthy credit score requires consistent effort and responsible financial behavior. In addition to managing hard credit pulls, there are several strategies you can implement to improve and protect your credit profile.

Pay Bills on Time: Timely payments are crucial for maintaining a good credit score. Set up automatic payments or reminders to ensure you never miss a payment deadline.

Monitor Credit Utilization: Keep your credit utilization below 30% to demonstrate responsible credit management. This shows lenders that you're not overextending yourself financially.

Additional Strategies

- Review your credit report annually

- Dispute errors on your credit report

- Limit the number of credit accounts you open

Common Misconceptions About Hard Credit Pulls

There are several misconceptions surrounding hard credit pulls and their impact on credit scores. Addressing these misconceptions can help you make informed decisions about your financial health.

Myth 1: All Credit Inquiries Impact Your Credit Score - Only hard inquiries affect your credit score. Soft inquiries, such as checking your own credit report, do not have any impact.

Myth 2: A Single Hard Inquiry Can Ruin Your Credit - While a hard inquiry can temporarily lower your credit score, its impact is usually minimal and short-lived. Maintaining good financial habits can offset any negative effects.

Other Common Misconceptions

- Rate shopping always results in multiple hard inquiries

- Closing old credit accounts improves your credit score

How to Check Your Credit Report

Regularly monitoring your credit report is essential for maintaining financial health. You can obtain a free copy of your credit report annually from each of the three major credit bureaus: Equifax, Experian, and TransUnion. Reviewing your credit report allows you to identify errors, detect fraudulent activity, and track the impact of hard credit pulls.

Additionally, many financial institutions and credit card companies offer free credit monitoring services. These services provide real-time updates on your credit report and alert you to any changes or suspicious activity.

Conclusion

In conclusion, understanding how long a hard credit pull lasts and its impact on your credit score is vital for maintaining financial stability. While hard inquiries can temporarily affect your credit rating, their impact is generally minimal and short-lived. By implementing responsible financial practices and managing credit applications wisely, you can protect your credit score and achieve long-term financial success.

We encourage you to take action by regularly monitoring your credit report, paying bills on time, and limiting unnecessary credit applications. Share your thoughts and experiences in the comments below, and don't forget to explore other informative articles on our website.